2023 Market Update

2023 Market Update

Given the start of this year, we decided it may be helpful to provide context on the year so far. Please find below a brief update on how we are seeing the state of the markets.

To the surprise of many investors, both the equity and fixed income markets have been off to a fast start in 2023 as major indices were up stronger than forecasted. Inversely, many investors were defensively positioned coming into the year with the uncertainty around whether the Fed could tame inflation without knocking the economy into recession. While the market has proven resilient so far, it is our view that it is still too early to signal ‘all clear’. With that, we wanted to recap the year and dive into the intricate web of the 2023 economic landscape.1

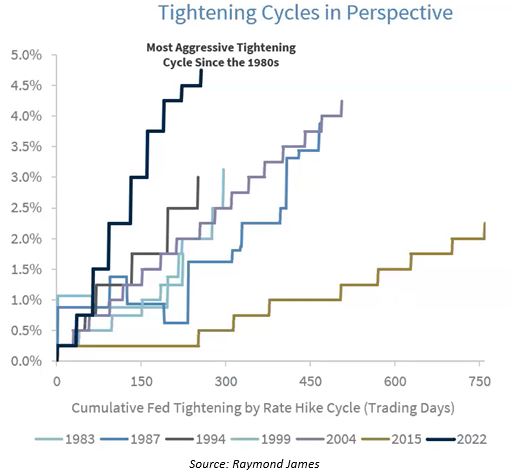

Going into 2023, markets were uneasy. The country was digesting one of the steepest and most aggressive rate-hiking cycles in history out of The Federal Reserve, as illustrated in the chart below (dark purple line on the left):

As you can see, this was the fastest and highest rate cycle in history, resulting in a 4.75% increase on the Fed Funds Rate over the course of 12 months. Going into 2022, investors anticipated a more gradual move such as the gold line on the right. These unexpected increases caused shockwaves throughout the system and negative asset prices across the board, resulting in the worst year ever for bonds at -16% and equities returning -19%.2 For example:

1. Equities: When interest rates are increased, this induces higher borrowing costs for businesses, compressed margins, and reduced earnings – a key driver to a stock’s price. This also results in higher costs to consumers, where it becomes more expensive to finance purchases and borrow money.

2. Fixed Income: When interest rates are increased, the price of existing bonds in the market place will decrease as new bonds are issued at higher interest rates. Although, the bonds that decreased in value will still mature at par of $1,000 per bond (assuming the company/institution meets its debt obligations), the investment would be at a loss if sold before then.3

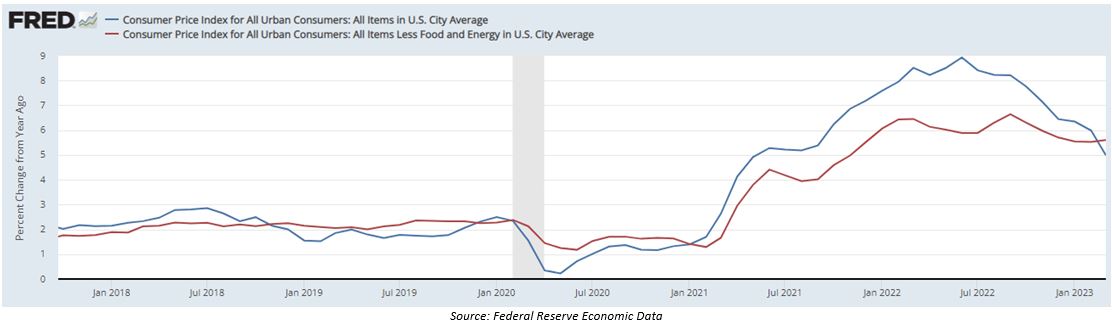

Thankfully, we saw these aggressive moves by the Fed pay off as the Consumer Price Index (CPI) came off its highs of 9.1% in June of 2022, and have continued to decrease. In this year’s January reading, we saw year-over-year changes of 6.3%, 6% in February, and 5% in March.

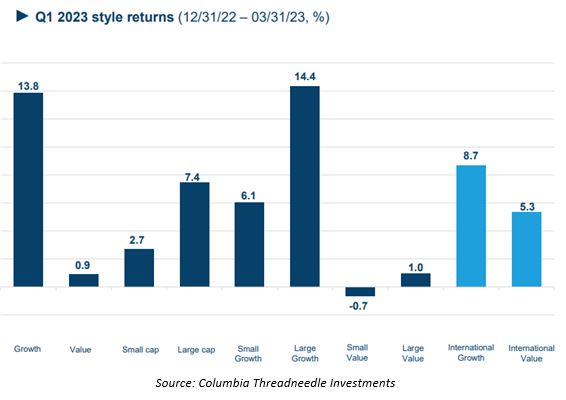

As inflation has continued its downward trajectory throughout the year, there has been positive sentiment in our view that the Fed 1) is on course for a successful “soft landing” of the economy and 2) would allow them to take their foot off the pedal and slow the pace of rate hikes or potentially pause. As a result, equity markets reacted positively on the expectations of lower rates. Most of the benefactors during the recent equity market rally have been in the same sectors that were hit the hardest in 2022, contrary to market expectations coming into the year.4

As you can see above, growth-heavy sectors (tech, communication services, consumer discretionary) vastly outperformed value (healthcare, financials, energy) as investors attempted to partake in the equity rally by flocking to larger, growth-oriented companies. While these returns are a welcomed sight, inflation is still at 5% year-over-year and The Fed has not committed to pausing or cutting interest rates. Ultimately, our view is the path forward is going to be extremely sensitive to economic data (inflation, jobs market) and Fed policy decisions. Until there is clarity and consistency in the aforementioned topics, we expect the volatility to remain.

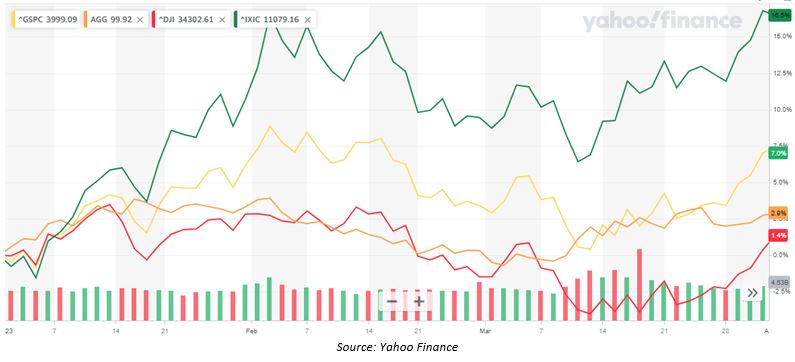

While equity market returns have been positive this year, it has been far from a slow and steady move higher. In the graph below, you will see the highs and lows throughout the quarter (1/1/2023 – 3/31/2023) of a few of the major US market indices6:

• NASDAQ (Green): 15.6%

• SP500 (Yellow): 7.8%

• Dow Jones Industrial Average (Red): 1.9%

• Aggregate Bond Index (Orange): 2.3%

As displayed in the graph above, markets have seesawed this year as it’s tried to price in changes with economic data and fed policy decisions. In January, there were positive returns for both equities and fixed income stemming from inflation data that proved it was continuing its trend downwards and market speculation that the Fed was nearing the end of its rate hike cycle.

Subsequentially, February was a different story as Fed chair, Jerome Powell, squashed out the chances of a pause on interest rate increases. As a result, asset prices compressed to account for a more restrictive Fed and the increased risk of a Fed-induced recession. As he states below:

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. In support of these goals, the Committee decided to raise the target range for the federal funds rate to 4-1/2 to 4-3/4 percent. The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time. In determining the extent of future increases in the target range, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments”

To begin March, there was selling pressure sparked by concerns over the banking and credit system – brought to light by the swift collapse of Silicon Valley Bank, Signature Bank, Credit Suisse and most recently First Republic Bank. The knee-jerk reaction in the market was to sell, but after the Fed stepped in to provide liquidity to banks that needed it and more due diligence was done on the root cause of these bank failures, the market reversed upwards.

The month of April remained relatively muted as there was no Federal Reserve meeting and the market continued to digest company earnings and regional bank headlines. Most recently, the Fed made the decision to increase interest rates another 0.25%, bringing the fed funds rate to 4.75-5.00%. It is our view that the Fed will likely pause on any additional rate hikes as they wait to see the impact of more restrictive monetary policy, as well monitoring the path of inflation.

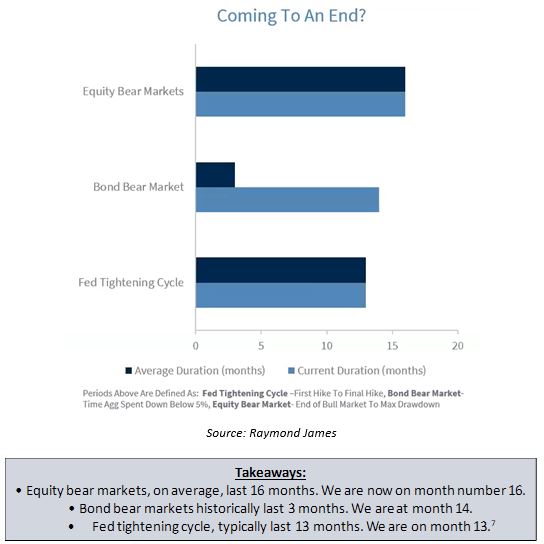

As of today, the markets continue to be on shaky footing with the number of uncertain variables in the system: inflation readings, Federal Reserve rate hikes, unemployment figures, regional bank concerns and geopolitical tensions. Raymond James’ analysts are forecasting a mild recession in the coming months as GDP is projected to be negative over the next two quarters and the heightened interest rates are felt throughout the system and the economy continues to slow. Fortunately, many are projecting a mild recession where most of the pain seems to be felt and priced into the markets for the most part. Here are a few stats to consider:

In summary, you will often hear the phrase “data dependent” within financial news outlets as the market continues to digest economic readings and headlines that are released daily. Due to this market environment and level of uncertainty of the direction of markets, there will continue to be bouts of volatility as headlines become available to the upside and downside. A couple things to keep in mind as we continue to weather this economic cycle:

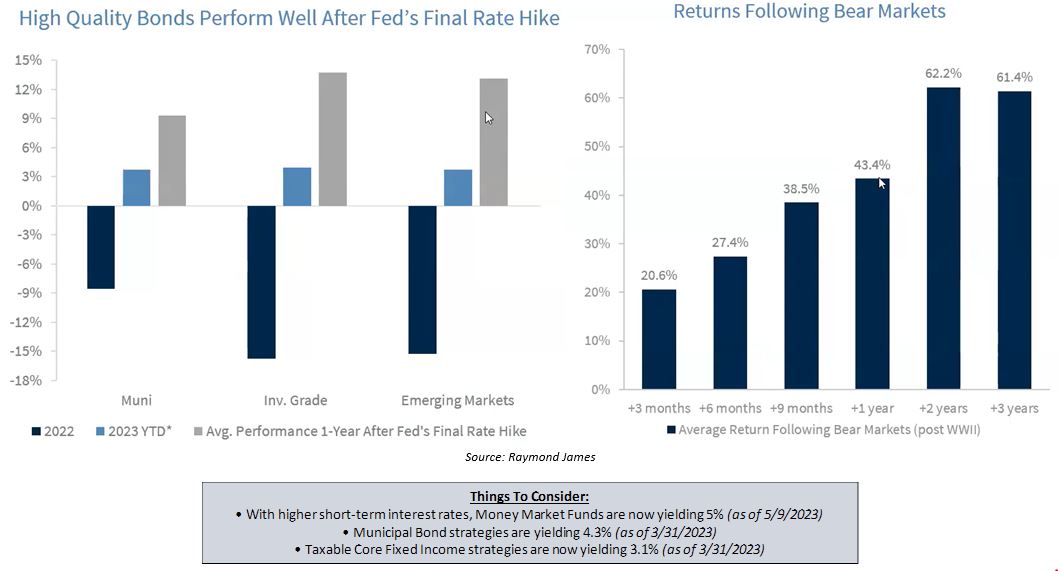

1. For those with a more shorter time horizon and risk-averse appetite, fixed income tends to outperform at the end of tightening (rising interest rates) cycles – first chart

2. And for those with longer time horizons, returns bode well for equities following a bear market cycle – second chart7

We hope you find this helpful in understanding how and why markets continue to move. If there is anything we can do on our end, such as revisiting your financial plan, investments, or fielding any questions you may have, please feel free to reach out.

Best,

Gary, Chris, Will, Matt, & Derrick

Sources:

- Welcome To Ten Themes For 2023 – Larry Adams

- 2023 Market Outlook

- How Do Interest Rates Effect The Stock Market

- Federal Reserve Economic Data

- Columbia Threadneedle Outlook & Opportunities – Q2 2023

- Yahoo Finance

- Quarterly Coordinates: Time Is On Our Side – 2Q 2023 Outlook

Disclosures:

Columbia Threadneedle Chart:

Growth represented by Russell 3000 Growth Index; value by Russell 3000 Value Index; small cap by Russell 2000 Index; large cap by Russell 1000 Index; small growth by Russell 2000 Growth Index; large growth by Russell 1000 Growth Index; small value by Russell 2000 Value Index; large value by Russell 1000 Value Index; international growth by MSCI ACWI ex USA Growth Index; and international value by MSCI ACWI ex USA Value Index.

Return Following Bear Markets Chart:

Equity data represented by SP500 Total Return Index.

Things To Consider Text Box:

Money Market Funds represented by Goldman Sachs Financial Square Government Fund (FGTXX).

Municipal Bond Strategies represented by Eagle Asset Management Municipal Managed Income Solutions SMA.

Taxable Core Plus Fixed Income represented by Federated Core Plus Income SMA.

The views expressed herein are those of the author and do not necessarily reflect the views of Steward Partners or its affiliates. All opinions are subject to change without notice. Neither the information provided nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. Past performance is no guarantee of future results.

Keep in mind that individuals cannot invest directly in any index, and index performance does not include transaction costs or other fees, which will affect actual investment performance. Individual investor's results will vary. Past performance does not guarantee future results. Future investment performance cannot be guaranteed, investment yields will fluctuate with market conditions.

For index definitions click here

Steward Partners Investment Solutions, LLC (“Steward Partners”), its affiliates and Steward Partners Wealth Managers do not provide tax or legal advice. You should consult with your tax advisor for matters involving taxation and tax planning and their attorney for matters involving trust and estate planning and other legal matters.

AdTrax 5671967.1 Exp 5/24